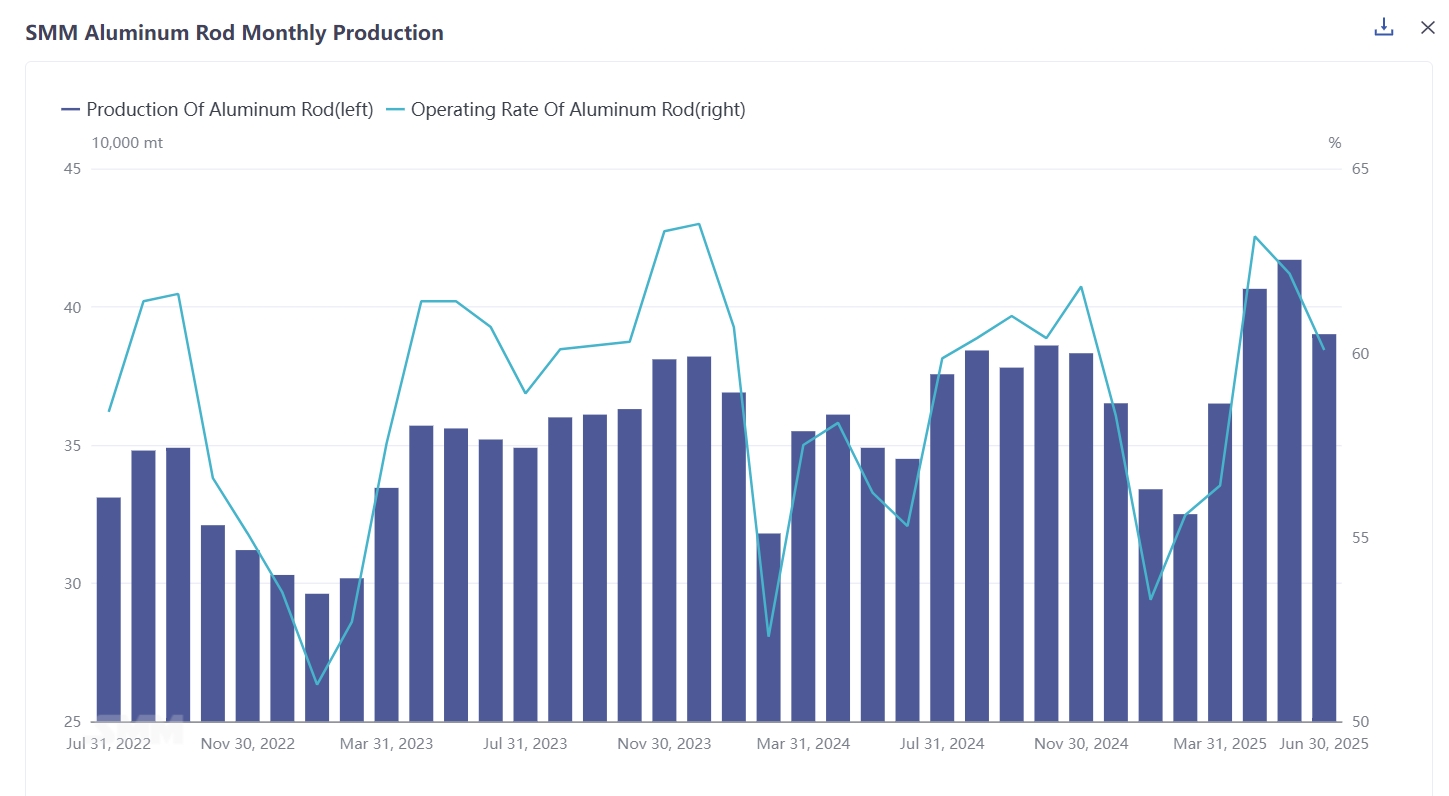

According to the latest monthly survey data from SMM, the total production of aluminum rods nationwide in June 2025 was 390,000 mt, a decrease of 27,000 mt from May. After adjusting for the number of days in the month, the operating rate of aluminum rod plants in June was recorded at 60%, down 2% MoM and up 5% YoY. Overall, despite weak downstream purchasing, in-plant inventory was in the initial stage of inventory buildup, coupled with the task of liquid aluminum alloying, the aluminum rod supply side remained at highs in June. However, as the off-season atmosphere in the downstream sector became increasingly pronounced, with market purchasing significantly weakening, many plants announced production cuts and maintenance of equipment in mid-to-late June. It is expected that there will be a pullback in the aluminum rod supply side in July, and the pressure of market supply surplus may ease slightly.

In terms of operating rates by region, all provinces showed a trend of declining operating rates. As a major production hub for aluminum rods, Shandong and Inner Mongolia regions recorded operating rates of 82.7% and 75.2%, respectively, with a slight MoM decline. Meanwhile, provinces such as Guangxi, Guizhou, Ningxia, and Qinghai also showed a downward trend in operating rates. By early-to-mid July, many aluminum rod plants reported increasing in-plant inventory pressure, while the sustained high aluminum prices suppressed consumption, and plants were about to enter the stage of production cuts and maintenance. Therefore, it is expected that provinces will still face downward pressure on operating rates in July.

According to SMM statistics, the in-plant inventory of aluminum rod plants accumulated for 9.2 days, an increase of 6.04 days from the previous month. In-plant inventory of aluminum rod plants showed an upward trend within the month due to weak downstream consumption. However, with many production cut expectations emerging from the supply side in July, the subsequent increase in supply may slow down, and it is expected that in-plant inventory of aluminum rods will operate within the range of 6-13 days in July.

In terms of specific processing fees, the monthly average ex-factory processing fee for 1A60 in Shandong region in June was recorded at 310 yuan/mt, a decrease of 221 yuan/mt from the previous month. The monthly average ex-factory processing fee in Henan region was recorded at 355 yuan/mt, a decrease of 160 yuan/mt from the previous month. The monthly average ex-factory processing fee in Inner Mongolia region was 212 yuan/mt, down 237.5 yuan/mt MoM. Among the three major trading hubs, the monthly average delivered processing fee in Hebei region was 302 yuan/mt, a decrease of 281 yuan/mt. The monthly average delivered processing fee in Jiangsu region was 382 yuan/mt, a decrease of 301 yuan/mt. The monthly average delivered processing fee in Guangdong region was 302.5 yuan/mt, a decrease of 281 yuan/mt. It is expected that processing fees in various regions will still face downward pressure in July, mainly due to the relative oversupply in the market and weak demand. The upside potential for aluminum rod processing fees is relatively limited, with low trading sentiment in the industry, and it is difficult to lift the center of processing fees in the short term. SMM believes that the performance of the aluminum rod market in June was not satisfactory. As aluminum rod manufacturers continued to operate at high capacity levels, in-plant inventory continued to accumulate. However, the sustained high aluminum prices suppressed downstream consumption, and coupled with the industry being in the midst of an off-season, weak demand resulted in a relative surplus in market supply, making it difficult for processing fees to improve. Therefore, considering the increasing trend of in-plant inventory and the off-season demand, it is expected that aluminum rod processing fees will continue to operate at low levels in the short term. From a medium and long-term perspective, downstream wire and cable enterprises are not short of backlog orders, and there will still be a concentrated delivery phase in H2, with rigid demand still able to support industry consumption. Despite the expectation of concentrated deliveries for downstream aluminum wire and cable, considering the accumulation of in-plant inventory, there may be a certain lag in the rebound cycle of aluminum rod processing fees.